Inland Revenue have recently announced this year’s livestock Herd Scheme Values and we think this is a great opportunity to update you on the latest movements. The Herd Scheme Values are the National Average Market Values as determined by a process involving a review of the livestock market as at 30 April.

Dairy Cattle

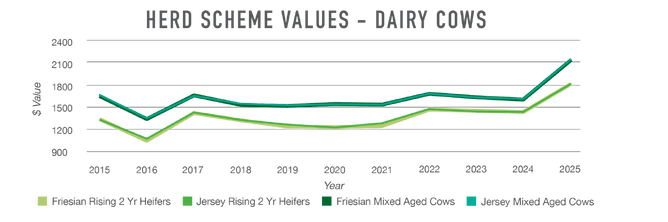

The values for dairy this year have seen a significant increase across both female and male classes. The increase can be attributed to very strong commodity prices for dairy products resulting in strong demand for dairy cattle. Strong commodity prices and the reframing or relaxation of some environmental factors have seen renewed interest in dairy conversions in parts of the South Island which may drive further demand.

A Mixed Age Dairy cow now has a National Average Market Value of $2,111 compared to $1,609 last year – a rise of 31.2%. Rising one and two-year heifers have increased in value by

49% and 27.4%, to $1,007 and $1,826 respectively.

The outlook for the farmgate milk price remains strong due to tight supply in the EU and Australia, robust demand and a weaker NZ dollar. On farm costs remain high but falling interest rates are easing financial pressures. We are unlikely to see the same level of increase in livestock values again next year with values close to the highs seen in 2008 and 2012.

Beef Cattle

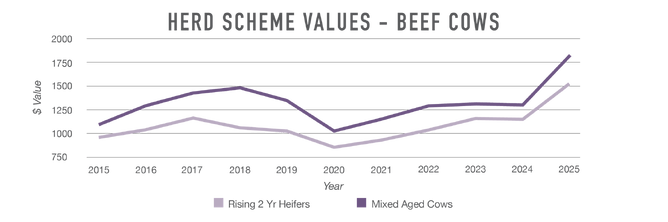

As with dairy values, beef values have risen strongly, on average a 35% increase to the highest values ever seen for Beef Cattle. Following weak commodity prices in the 2023-24 year we have seen a much stronger red meat commodity market in the 2024-25 year. Farmgate beef prices are over 40% higher than the 5-year average, fuelled by strong US demand and a tight global red meat supply.

Ongoing land conversion to forestry will continue to constrain supply, with beef production expected to decline on the back of a smaller national herd size. If demand continues as expected farmgate prices are expected to hold the current high values.

The beef industry continues to be at risk from changes in environmental policies, many of which remain unsettled at Local and Central Government levels. As a consequence, we are likely to continue to see volatility in beef cattle values in the future.

Sheep

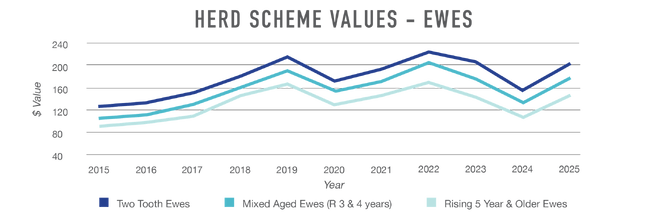

Similar to beef values, sheep values have risen strongly, on average a 38% increase, erasing the 2024 fall in values. Increased values are on the back of strong global demand, from the UK, EU and US, even though demand in China has been weak.

Total sheep numbers continue to decline, putting pressure on processing numbers, which further tightens supply. This coupled with further land conversion continues to put pressure on the industry. High debt levels are also encouraging farmers to exit the industry in favour of land conversion, which will further limit supply and likely see further processor closures as numbers fall.

Wool markets have improved, with 8-year highs being achieved for crossbred fleece. There is also renewed optimism driven by consumer demand for natural fibres, including Government led initiatives mandating the use of wool in public infrastructure.

Shearing costs remain high relative to wool prices which continues to fuel interest in self-shedding sheep breeds.

Goats

Goat values aside from breeding bucks declined by 12.5% on average for the 2025 year.

Challenges continue to exist for the milking goat industry as demand is matched against supply and the significant costs associated with establishing on farm infrastructure.

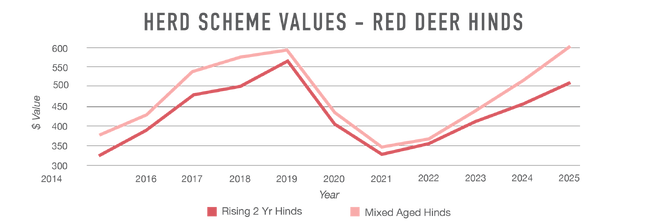

Deer

Deer values saw further recovery from the low values of 2021 with an average 15% increase in values for Red Deer, Wapiti, and related breeds. Other breeds bucked that trend with values falling 6.7% on average.

Strong returns continue to be forecast with retail demand in the US and Canada continuing to grow.

International trophy hunting tourism continues to rebound following Covid-19 with strong interest from US and European hunters.